Trainer Joe: Get DeFit — Lending Part 1

Welcome to DeFit Bootcamp, with Trainer Joe

This is the 1st of a 5 part series to help you bulk out your DeFit knowledge and get some serious kudos amongst the community

Those who train with Joe will be rewarded with an exclusive Discord badger of honor: ‘DeFit’

🏃♂️ Session 1

Today’s session will help you build your knowledge of DeFi Lending protocols. Lending protocols are platforms that enable everyone to earn interest on tokens they supply and also take loans by borrowing additional tokens. This is all carried out over a frictionless, peer 2 peer infrastructure.

🏋️♂️ 1st Rep: Difference between APY and APR

Annual Percentage Yield (APY): APY accrues and compounds daily

Annual Percentage Rate (APR): APR accrues, but does not compound daily

Lending

Lending your tokens is a great way to earn interest on assets that would otherwise sit in your wallet ‘doing nothing’. Lending tokens is similar to depositing cash into a savings account at a bank. You can deposit your tokens into a Lending protocol, like Banker Joe, and earn compounding daily interest.

🏋️♂️ 2nd Rep: Deposit APY

If you Lend AVAX, you receive Interest in AVAX tokens.

This interest you receive is represented as a % return ‘Deposit APY’

Borrowing

Borrowing tokens from a Lending protocol is similar to taking out a loan at a bank. Before you can take out a loan, you need some form of ‘collateral’, typically a signed agreement with payback terms. On a permissionless, P2P Lending protocol, to Borrow tokens first you will need to deposit tokens, as collateral. Once you have deposited your collateral, you can then borrow tokens. Borrowing tokens is not free, you will pay daily Interest on what you borrow.

🏋️♂️ 3rd Rep: Borrow APY

If you Borrow AVAX, you pay Interest in AVAX tokens

This cost to you is represented in the form of ‘Borrow APY %’

Lending & Borrowing

Combining both Lending & Borrowing activities together, is essentially the core service of a Lending Protocol, like Banker Joe. Lending Protocols facilitate the transaction, between two anonymized users. For users of Banker Joe, if you participate in Lending &/Or Borrowing, you will see two metrics that provide you with a summed position of your portfolio, Net APY and Rewards APY.

🏋️♂️ 4th Rep: Net APY

Net APY is the net position on your interest & borrowing activity. The figure represents your expected return over the year.

Sum: Deposit APY — Borrowing APY = Net APY

Weighted average calculation

🏋️♂️ 5th Rep: Reward APR

Reward APR is the additional incentive rewarded when using Banker Joe. These are paid out in either Joe Tokens or Avax Tokens. You can claim rewards anytime.

This is a weighted average calculation

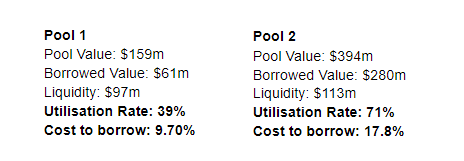

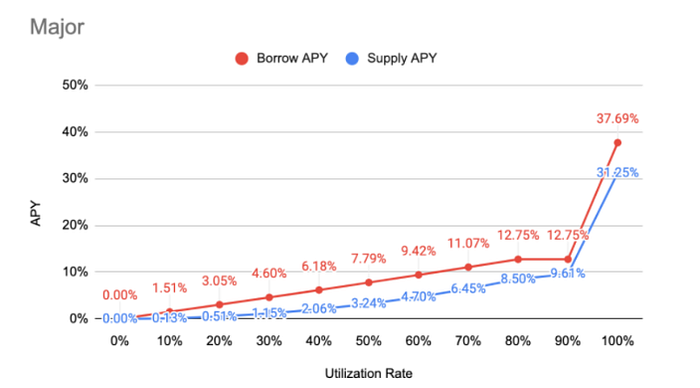

Utilization Ratio

The Interest rates on Banker Joe are set using an algorithmic calculation, referred to as the Utilisation Ratio, a model introduced by Compound.

Utilisation Rate = Borrowing / (Liquidity + Borrowing) x 100

Interest rates set are defined by the Liquidity Supplied and Borrowed for each token. Essentially, this is simple economics of Supply and Demand at work. Higher liquidity Supplied, will decrease the cost to Borrow and therefore incentivize more users to Borrow and vice versa.

To help manage Liquidity on the Lending protocol, the Interest Rate model sets out the Utilisation Ratio over 3 slopes. These slopes define the multiplier to the underlying Interest rate calculation and help the protocol manage risk of the underlying assets.

The Utilisation Ratio slopes are:

- 0–80%

- 80–90%

- 90–100% (Interest Rates dramatically increase at this slope)

🏋️♂️ 6th Rep: Utilisation Rate

The % of the Liquidity pool supplied for the Token

🏋️♂️ 7th Rep: Utilisation Rate Calculation

Divide the Borrowed amount by the Total Supplied to the Liquidity Pool

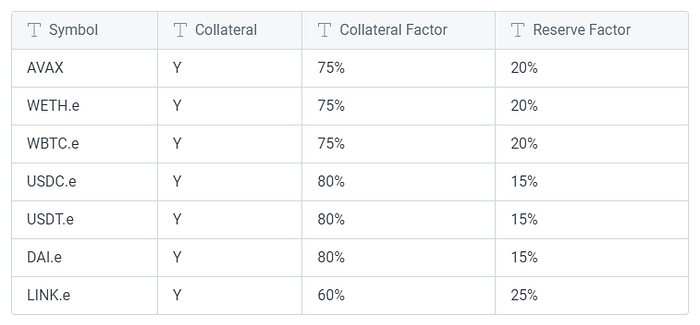

Collateral Factor / Loan to Value (LTV)

The Collateral Factor represents the % that can be Borrowed against the value of the Deposits that have been supplied.

Collateral Factor = (Borrowing / Collateral Value) * 100

Example

- USDC.e Collateral Factor: 80%

- Deposit: $1k

- Borrow Limit: $400 (50% of Collateral Factor)

🏋️♂️ 8th Rep: Collateral Factor / Loan to Value (LTV)

The collateral Factor determines the max amount of collateral you can borrow against your deposited value.

Reserve Factor

The Reserve factor is a percentage of the interest accrued by the Lending Protocol, that is paid by Borrowers. This is set aside by the Lending Protocol (Banker Joe) to offset Protocol risk, such as a shortfall event.

To calculate the reserve factor’s value, a set percentage is taken off the value of your interest.

- Reserve Factor: 20%

- Calculation: 20% of $100

- Reserve Value: $20

- Total after reserve value deductions: $80

Reserve factors are configured differently for each Token. This is to account for the different levels of risk for each token as well as the liquidity. Banker Joe has the following Reserve factors

🏋️♂️ 9th Rep: Reserve Factor

The Reserve Factor is the % of Interest accrued, paid to the Lending Protocol to help protect the platform from losses due to an event such as a shortfall.

🏋️♂️ 10th Rep: Token Reserve Factors

Tokens on Banker Joe have different Reserve Factors set, this is configured specifically to help manage underlying Token Risk.

_____________________________________________

📖 Want extra information?

Banker Joe Whitepaper

_____________________________________________

Congratulations — Session Complete 🥇

Now it’s time to flex your muscles and lock in those gains.

Take on the challenge and get DeFit.

Complete the Quiz to build your progress towards the DeFit badge of honor.

🧠 Good luck! : Quiz link

About Trader Joe

Trader Joe is a one-stop-shop decentralized trading platform native to the Avalanche blockchain. Trader Joe builds fast, securely and aims to serve the community at the frontier of DeFi. The long-term vision of the team is to make Trader Joe an R&D-focused platform for new DeFi primitives not yet seen on any blockchain.